Understanding Your Home Loan: The Comprehensive Guide to Correct Assessment

Breaking down your mortgage can seem like traversing a complicated labyrinth, especially with the myriad of numbers and jargon involved. HipoteCalc find themselves lost in a pool of interest rates, loan terms, and hidden fees. It's essential to comprehend the full scope of what you're agreeing to, ensuring that you are aware precisely how much you will owe over the life of your loan.

One of the most effective tools you can employ in this journey is a mortgage calculator. This convenient device helps you analyze the expenses associated with your mortgage, allowing you to see not just the monthly dues but also how various elements like interest rates and loan lengths affect your overall financial commitment. By leveraging the power of accurate calculations, you can take informed decisions and take control of your mortgage.

Grasping Mortgage Principles

A mortgage is a loan uniquely crafted to help people buy a house. It involves borrowing a substantial sum of money from a lender, which you then repay over a period, typically through monthly installments. The house it acts as collateral for the debt, meaning if you struggle to make repayments, the lender can take ownership of the property.

When you apply for a home loan, several key terms come into play. The principal refers to the initial loan amount, while the interest rate is the fee of taking that money, expressed as a proportion. Home loans also entail different other factors, such as mortgage term, which is the total duration you have to pay off the debt, and regular payments that consist of both principal and interest, along with taxes and homeowners insurance.

Comprehending these principles is crucial for any homebuyer. It enables you to understand how much you'll be spending each month and the total cost of your loan over its duration. Utilizing a mortgage estimator can make easier this task, providing a clearer picture of your finances and assisting you make educated decisions about your future home.

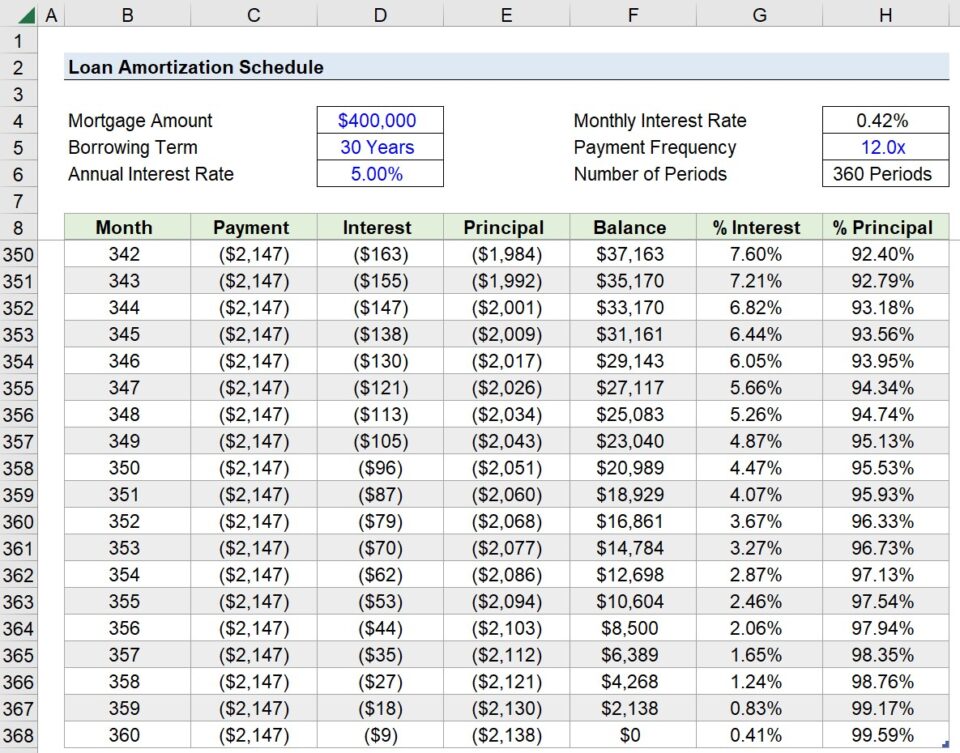

How to Use a Home Calculator

Utilizing a mortgage calculating tool is a straightforward process that can help you grasp the monetary consequences of your home acquisition. Start by inputting the loan amount, being the total price of the home less your down payment. This amount represents the principal that you will need to acquire. Most calculators also let you to customize the loan term, usually ranging from 15 to 30 years, so you can see how various durations affect your monthly payments.

Next, enter the interest rate for your mortgage. This is the rate your lender will charge for borrowing the money, and it can greatly impact your monthly payment and the overall amount you will spend over the life of the loan. Mortgage calculators often have predefined interest rates, but they also allow you to enter a custom rate if you have previously secured one from a lender. Keep in mind, even a slight change in the interest rate can lead to substantial changes in your monthly and total payments.

Finally, some mortgage calculators offer additional features that help you consider property taxes, homeowner's insurance, and private mortgage insurance, if applicable. By adding these expenses, you can get a more comprehensive understanding of your total monthly payment. Once you have filled in all the required fields, click the calculate button to view your results. This gives you a clearer vision of what to expect financially when considering a mortgage.

Common Mistakes in Home Loan Estimates

One frequent mistake in home loan calculations is neglecting to account for all expenses associated with the loan. Many home buyers focus solely on the main amount and finance payments, overlooking factors such as taxes on the property, homeowners insurance, and loan insurance. These additional costs can significantly affect the total monthly payment, leading to an inaccurate understanding of financial obligations. It is essential to use a comprehensive mortgage calculator that takes into account all these factors to get a clearer picture of what to anticipate.

Another frequent error is using the incorrect interest rate in calculations. Borrowers may miss the distinction between static and variable rates or forget to consider the APR, which encompasses extra fees beyond just the nominal interest rate. Using a mortgage calculator with incorrect interest information can lead to misguided expectations regarding monthly payments and overall mortgage affordability. Always check the current rates and use them in your estimations to guarantee accuracy.

Lastly, many individuals undervalue the importance of the loan term when calculating their mortgage. A widespread misconception is that a longer term greatly eases monthly payments without appreciating the long-term financial consequence. While lengthening the term can reduce monthly costs, it often results in paying more interest over the life of the loan. Borrowers should carefully evaluate how the term influences both their monthly budget and the overall cost of the mortgage to make wise decisions that align with their financial goals.